At the end of this article, my goal is to convince you that: if you need to

use random numbers, you should consider using

scipy.stats.qmc

instead of

np.random.

In the following, we assume that SciPy, NumPy and Matplotlib are installed and imported:

import numpy as np

from scipy.stats import qmc

import matplotlib.pyplot as pltNote that no seeding is used in these examples. This will be the topic of another article: seeding should only be used for testing purposes.

So what are Monte Carlo (MC) and Quasi-Monte Carlo (QMC)?

Monte Carlo (MC)#

MC methods are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results. The underlying concept is to use randomness to solve problems that might be deterministic in principle. They are often used in physical and mathematical problems and are most useful when it is difficult or impossible to use other approaches. MC methods are mainly used in three classes of problem: optimization, numerical integration, and generating draws from a probability distribution.

Put simply, this is how you would usually generate a sample of points using MC:

rng = np.random.default_rng()

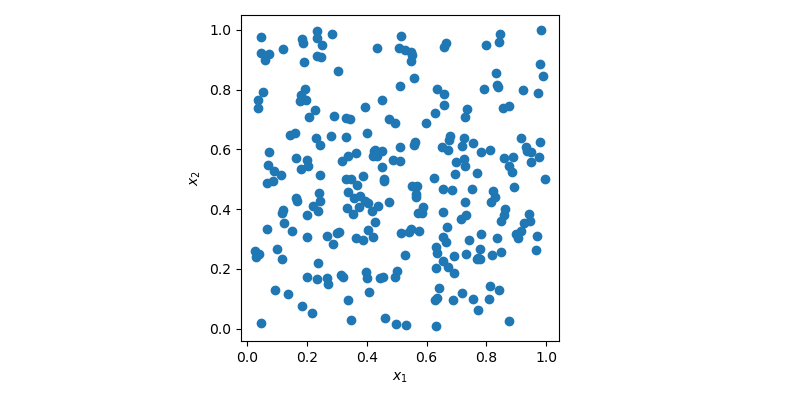

sample = rng.random(size=(256, 2))In this case, sample is a 2-dimensional array with 256 points which can be

visualized using a 2D scatter plot.

In the plot above, points are generated randomly without any knowledge about previously drawn points. It is clear that some regions of the space are left unexplored while other regions have clusters. In an optimization problem, it could mean that you would need to generate more sample to find the optimum. Or in a regression problem, you could also overfit a model due to some cluster of points.

Generating random numbers is a more complex problem than it sounds. Simple MC methods are designed to sample points to be independent and identically distributed (IID).

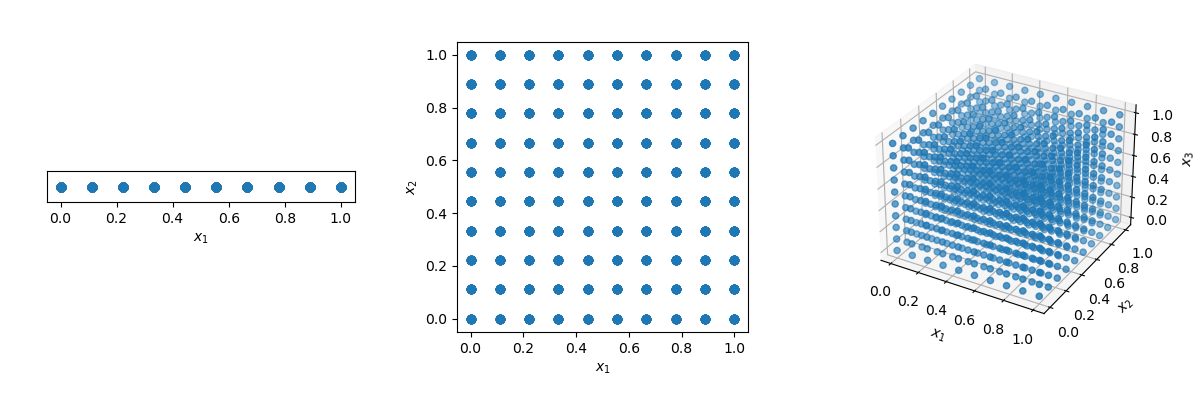

One could think that the solution is just to use a grid! But look what happens if we have a distance of 0.1 between points in the unit-hypercube ( with all bounds ranging from 0 to 1).

disc = 10

x1 = np.linspace(0, 1, disc)

x2 = np.linspace(0, 1, disc)

x3 = np.linspace(0, 1, disc)

x1, x2, x3 = np.meshgrid(x1, x2, x3)The number of points required to fill the unit interval would be 10. In a 2-dimensional hypercube the same spacing would require 100, and in 3 dimensions 1,000 points. As the number of dimensions grows, the number of samples which is required to fill the space rises exponentially as the dimensionality of the space increases. This exponential growth is called the curse of dimensionality.

Quasi-Monte Carlo (QMC)#

To mitigate the curse of dimensionality, you could decide to randomly remove points from the sample or randomly sample in n-dimension. In both cases, this will need to empty regions and clusters of points elsewhere.

Quasi-Monte Carlo (QMC) methods have been created specifically to answer this problem. As opposed to MC methods, QMC methods are deterministic. Which means that the points are not IID, but each new point knows about previous points. The result is that we can construct samples with good coverage of the space.

Deterministic does not mean that samples are always the same. the sequences can be scrambled.

Starting with version 1.7, SciPy provides QMC methods in

scipy.stats.qmc.

Let’s generate 2 samples with MC and a QMC method named Sobol’.

n, d = 256, 2

rng = np.random.default_rng()

sample_mc = rng.random(size=(n, d))

qrng = qmc.Sobol(d=d)

sample_qmc = qrng.random(n=n)A very similar interface, but as seen below, with radically different results.

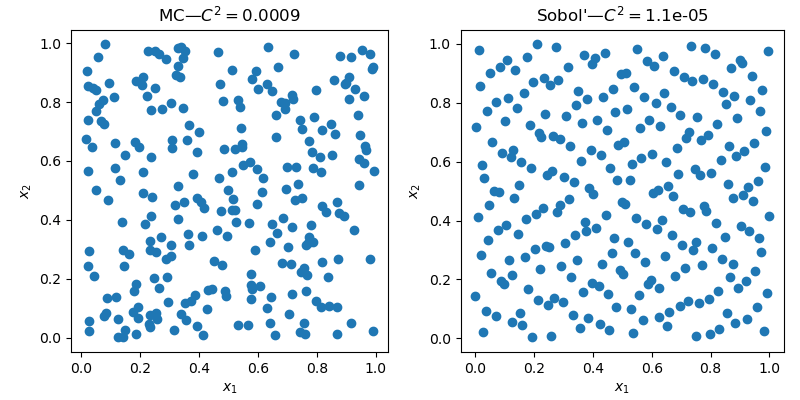

The 2D space clearly exhibit less empty areas and less clusters with the QMC sample.

Quality?#

Beyond the visual improvement of quality, there are metrics to assess the quality of a sample. Geometrical criteria are commonly used, one can compute the distance (L1, L2, etc.) between all pairs of points. But there are also statistical criteria such as: the discrepancy.

qmc.discrepancy(sample_mc)

# 0.0009

qmc.discrepancy(sample_qmc)

# 1.1e-05The lower the value, the better the quality.

Convergence#

If this still does not convince you, let’s look at a concrete example: integrating a function. Let’s look at the mean of the squared sum in 5 dimensions:

$$f(\mathbf{x}) = \left( \sum_{j=1}^{5}x_j \right)^2,$$

with $x_j \sim \mathcal{U}(0,1)$. It has a known mean value, $\mu = 5/3+5(5-1)/4$. By sampling points, we can compute that mean numerically.

The samplings are done 99 times and averaged. The variance is not reported for simplicity, just know that it’s guaranteed to be lower with QMC than with MC.

dim = 5

ref = 5 / 3 + 5 * (5 - 1) / 4

n_conv = 99

ns_gen = 2 ** np.arange(4, 13)

def func(sample):

# dim 5, true value 5/3 + 5*(5 - 1)/4

return np.sum(sample, axis=1) ** 2

def conv_method(sampler, func, n_samples, n_conv, ref):

samples = [sampler(n_samples) for _ in range(n_conv)]

samples = np.array(samples)

evals = [np.sum(func(sample)) / n_samples for sample in samples]

squared_errors = (ref - np.array(evals)) ** 2

rmse = (np.sum(squared_errors) / n_conv) ** 0.5

return rmse

# Analysis

sample_mc_rmse = []

sample_sobol_rmse = []

rng = np.random.default_rng()

for ns in ns_gen:

# Monte Carlo

sampler_mc = lambda x: rng.random((x, dim))

conv_res = conv_method(sampler_mc, func, ns, n_conv, ref)

sample_mc_rmse.append(conv_res)

# Sobol'

engine = qmc.Sobol(d=dim)

conv_res = conv_method(engine.random, func, ns, 1, ref)

sample_sobol_rmse.append(conv_res)

sample_mc_rmse = np.array(sample_mc_rmse)

sample_sobol_rmse = np.array(sample_sobol_rmse)

# Plot

fig, ax = plt.subplots(figsize=(4, 4))

ax.set_aspect("equal")

# MC

ratio = sample_mc_rmse[0] / ns_gen[0] ** (-1 / 2)

ax.plot(ns_gen, ns_gen ** (-1 / 2) * ratio, ls="-", c="k")

ax.scatter(ns_gen, sample_mc_rmse, label="MC: np.random")

# Sobol'

ratio = sample_sobol_rmse[0] / ns_gen[0] ** (-2 / 2)

ax.plot(ns_gen, ns_gen ** (-2 / 2) * ratio, ls="-", c="k")

ax.scatter(ns_gen, sample_sobol_rmse, label="QMC: qmc.Sobol")

ax.set_xlabel(r"$N_s$")

ax.set_xscale("log")

ax.set_xticks(ns_gen)

ax.set_xticklabels([rf"$2^{{{ns}}}$" for ns in np.arange(4, 13)])

ax.set_ylabel(r"$\log (\epsilon)$")

ax.set_yscale("log")

ax.legend(loc="upper right")

fig.tight_layout()

plt.show()

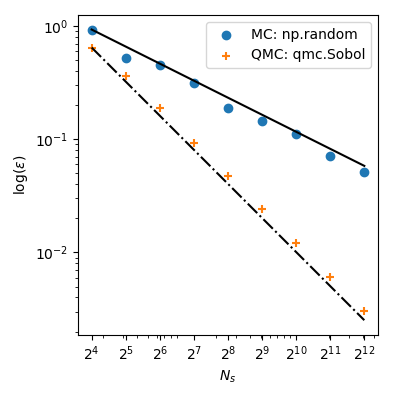

With MC the approximation error follows a theoretical rate of $O(n^{-1/2})$. But, QMC methods have better rates of convergence and achieve $O(n^{-1})$ for this function–and even better rates on very smooth functions.

This means that using $2^8=256$ points from Sobol’ leads to a lower error than using $2^{12}=4096$ points from MC! When the function evaluation is costly, it can bring huge computational savings.

Sampling from any distribution (advanced)#

But there is more! Another great use of QMC is to sample arbitrary

distributions. In SciPy 1.8, there are new classes of

samplers

that allow you to sample from any custom distribution. And some of

these methods can use QMC with a qrvs method:

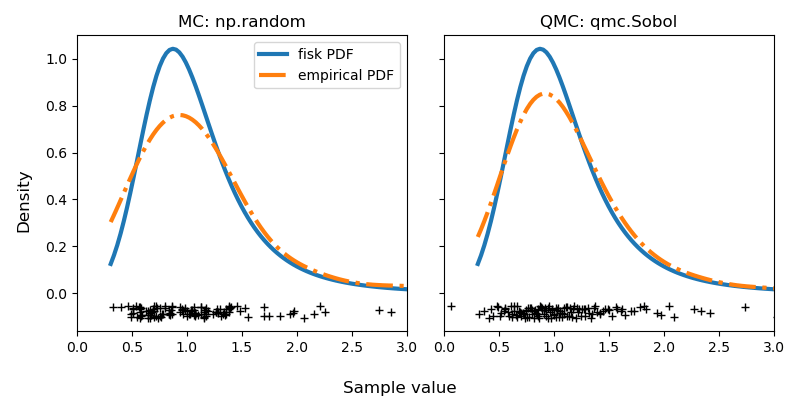

Here is an example with a distribution from SciPy: fisk. We generate

a MC sample from the distribution (either directly from the distribution with

fisk.rvs or using NumericalInverseHermite.rvs) and another sample with

QMC using NumericalInverseHermite.qrvs.

import scipy.stats as stats

from scipy.stats import sampling

# Any distribution

c = 3.9

dist = stats.fisk(c)

# MC

rng = np.random.default_rng()

sample_mc = dist.rvs(128, random_state=rng)

# QMC

rng_dist = sampling.NumericalInverseHermite(dist)

# sample_mc = rng_dist.rvs(128, random_state=rng) # MC alternative same as above

qrng = qmc.Sobol(d=1)

sample_qmc = rng_dist.qrvs(128, qmc_engine=qrng)Let’s visualize the difference between MC and QMC by calculating the empirical Probability Density Function (PDF). The QMC results are clearly superior to MC.

# Visualization

fig, axs = plt.subplots(1, 2, sharey=True, sharex=True, figsize=(8, 4))

x = np.linspace(dist.ppf(0.01), dist.ppf(0.99), 100)

pdf = dist.pdf(x)

delta = np.max(pdf) * 5e-2

samples = {"MC: np.random": sample_mc, "QMC: qmc.Sobol": sample_qmc}

for ax, sample in zip(axs, samples):

ax.set_title(sample)

ax.plot(x, pdf, "-", lw=3, label="fisk PDF")

ax.plot(samples[sample], -delta - delta * np.random.random(128), "+k")

kde = stats.gaussian_kde(samples[sample])

ax.plot(x, kde(x), "-.", lw=3, label="empirical PDF")

# or use a histogram

# ax.hist(sample, density=True, histtype='stepfilled', alpha=0.2)

ax.set_xlim([0, 3])

axs[0].legend(loc="best")

fig.supylabel("Density")

fig.supxlabel("Sample value")

fig.tight_layout()

plt.show()

Careful readers will note that there is no seeding. This is intentional as noted at the beginning of this article. You might run this code again and have better results with MC. But only sometimes. And that’s exactly my point. On average, you are guaranteed to have more consistent results with a better quality using QMC. I invite you to try it and see for yourself!

Conclusion#

I hope that I convinced you to use QMC the next time you need random numbers. QMC is superior to MC, period.

There is an extensive body of literature and rigorous proofs. One reason MC is still more popular is that QMC is harder to implement and, depending on the method, there are rules to follow.

Take the Sobol’ method we used: you must use exactly $2^n$ sample. If you don’t do it, you will break some properties and end up having the same performance than MC. This is why some people argue that QMC is not better: they simply don’t use the methods properly, hence fail to see any benefits and conclude that MC is “enough”.

In

scipy.stats.qmc,

we went to great lengths to explain how to use the methods, and we added some

explicit warnings to make the methods accessible and useful to

everyone.